In a previous article, I looked at 93 measurements from the ANSUR-II dataset and found that ear protrusion is not correlated with any other measurement. In a followup article, I used principle component analysis to explore the correlation structure of the measurements, and found that once you have exhausted the information encoded in the most obvious measurements, the ear-related measurements are left standing alone.

I have a conjecture about why ears are weird: ear growth might depend on idiosyncratic details of the developmental environment — so they might be like fingerprints. Recently I discovered a hint that supports my conjecture.

This Veritasium video explains how we locate the source of a sound.

In general, we use small differences between what we hear in each ear — specifically, differences in amplitude, quality, time delay, and phase. That works well if the source of the sound is to the left or right, but not if it’s directly in front, above, or behind — anywhere on vertical plane through the centerline of your head — because in those cases, the paths from the source to the two ears are symmetric.

Fortunately we have another trick that helps in this case. The shape of the outer ear changes the quality of the sound, depending on the direction of the source. The resulting spectral cues makes it possible to locate sources even when they are on the central plane.

The video mentions that owls have asymmetric ears that make this trick particularly effective. Human ears are not as distinctly asymmetric as owl ears, but they are not identical.

And now, based on the Veritasium video, I suspect that might be a feature — the shape of the outer ear might be unpredictably variable because it’s advantageous for our ears to be asymmetric. Almost everything about the way our bodies grow is programmed to be as symmetric as possible, but ears might be programmed to be different.

An article in a recent issue of The Economist suggests, right in the title, “Investors should avoid a new generation of rip-off ETFs”. An ETF is an exchange-traded fund, which holds a collection of assets and trades on an exchange like a single stock. For example, the SPDR S&P 500 ETF Trust (SPY) tracks the S&P 500 index, but unlike traditional index funds, you can buy or sell shares in minutes.

There’s nothing obviously wrong with that – but as an example of a “rip-off ETF”, the article describes “defined-outcome funds” or buffer ETFs, which “offer investors an enviable-sounding opportunity: hold stocks, with protection against falling prices. All they must do is forgo annual returns above a certain level, often 10% or so.”

That might sound good, but the article explains, “Over the long term, they are a terrible deal for investors. Much of the compounding effect of stock ownership comes from rallies.”

To demonstrate, they use the value of the S&P index since 1980: “An investor with returns capped at 10% and protected from losses would have made a real return of 403% over the period, a fraction of the 3,155% return offered by just buying and holding the S&P 500.”

So that sounds bad, but returns from 1980 to the present have been historically unusual. To get a sense of whether buffer ETFs are more generally a bad deal, let’s get a bigger picture.

The MeasuringWorth Foundation has compiled the value of the Dow Jones Industrial Average at the end of each day from February 16, 1885 to the present, with adjustments at several points to make the values comparable. The series I collected starts on February 16, 1885 and ends on August 30, 2024. The following cells download and read the data.

To compute annual returns, we’ll start by selecting the closing price on the last trading day of each year (dropping 2024 because we don’t have a complete year).

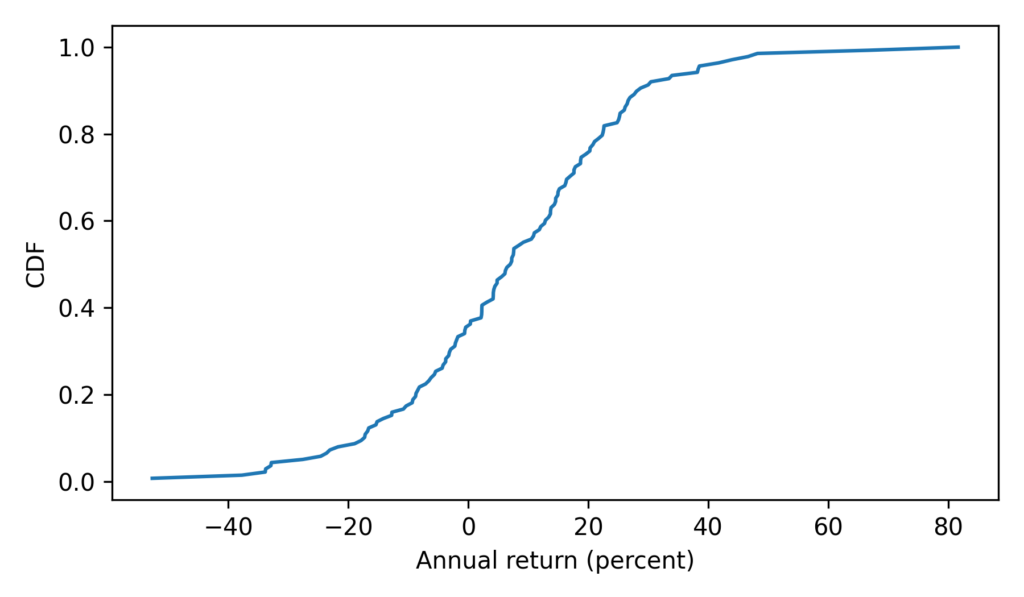

Looking at the years with the biggest losses and gains, we can see that most of the extremes were before the 1960s – with the exception of the 2008 financial crisis.

annual.dropna().sort_values(by='Return')

DJIA

Ratio

Return

Date

1931

77.9000

0.473326

-52.667396

1907

43.0382

0.622683

-37.731743

2008

8776.3900

0.661629

-33.837097

1930

164.5800

0.662347

-33.765293

1920

71.9500

0.670988

-32.901240

…

…

…

…

1954

404.3900

1.439623

43.962264

1908

63.1104

1.466381

46.638103

1928

300.0000

1.482213

48.221344

1933

99.9000

1.666945

66.694477

1915

99.1500

1.816599

81.659949

138 rows × 3 columns

Here’s what the distribution of annual returns looks like.

With this function, we can replicate the analysis The Economist did with the S&P 500. Here are the results for the DJIA from the beginning of 1980 to the end of 2023.

A buffer ETF over this period would have grown by a factor of more than 15 in nominal dollars, with no risk of loss. But an index fund would have grown by a factor of almost 45. So yeah, the ETF would have been a bad deal.

However, if we go back to the bad old days, an investor in 1900 would have been substantially better off with a buffer ETF held for 43 years – a factor of 7.2 compared to a factor of 2.8.

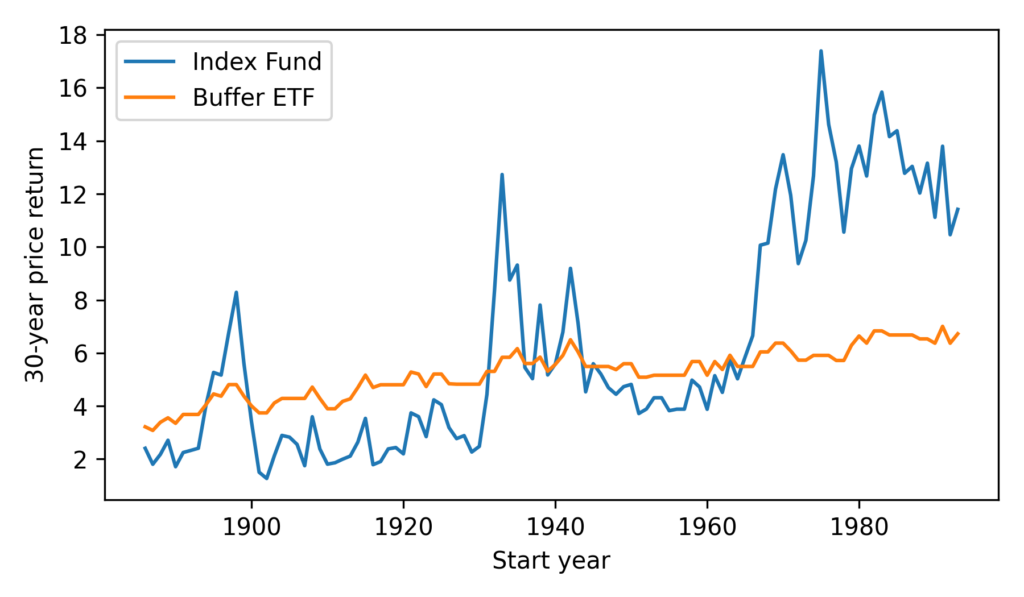

It seems we can cherry-pick the data to make the comparison go either way – so let’s see how things look more generally. Starting in 1886, we’ll compute price returns for all 30-year intervals, ending with the interval from 1993 to 2023.

The buffer ETF performs as advertised, substantially reducing volatility. But it has only occasionally been a good deal, and not in my lifetime.

According to ChatGPT, the primary reasons for strong growth in stock prices since the 1960s are “technological advancements, globalization, financial market innovation, and favorable monetary policies”. If you think these elements will generally persist over the next 30 years, you might want to avoid buffer ETFs.